When it comes to protecting your car, choosing the right comprehensive car cover can feel overwhelming. You want full protection without overpaying, but how do you know which policy truly fits your needs?

This guide will help you compare comprehensive car cover options side by side, so you can see what each plan offers and find the best value for your money. By the end, you’ll feel confident that your car—and your wallet—are both well protected.

Let’s dive in and discover how to get the coverage you deserve.

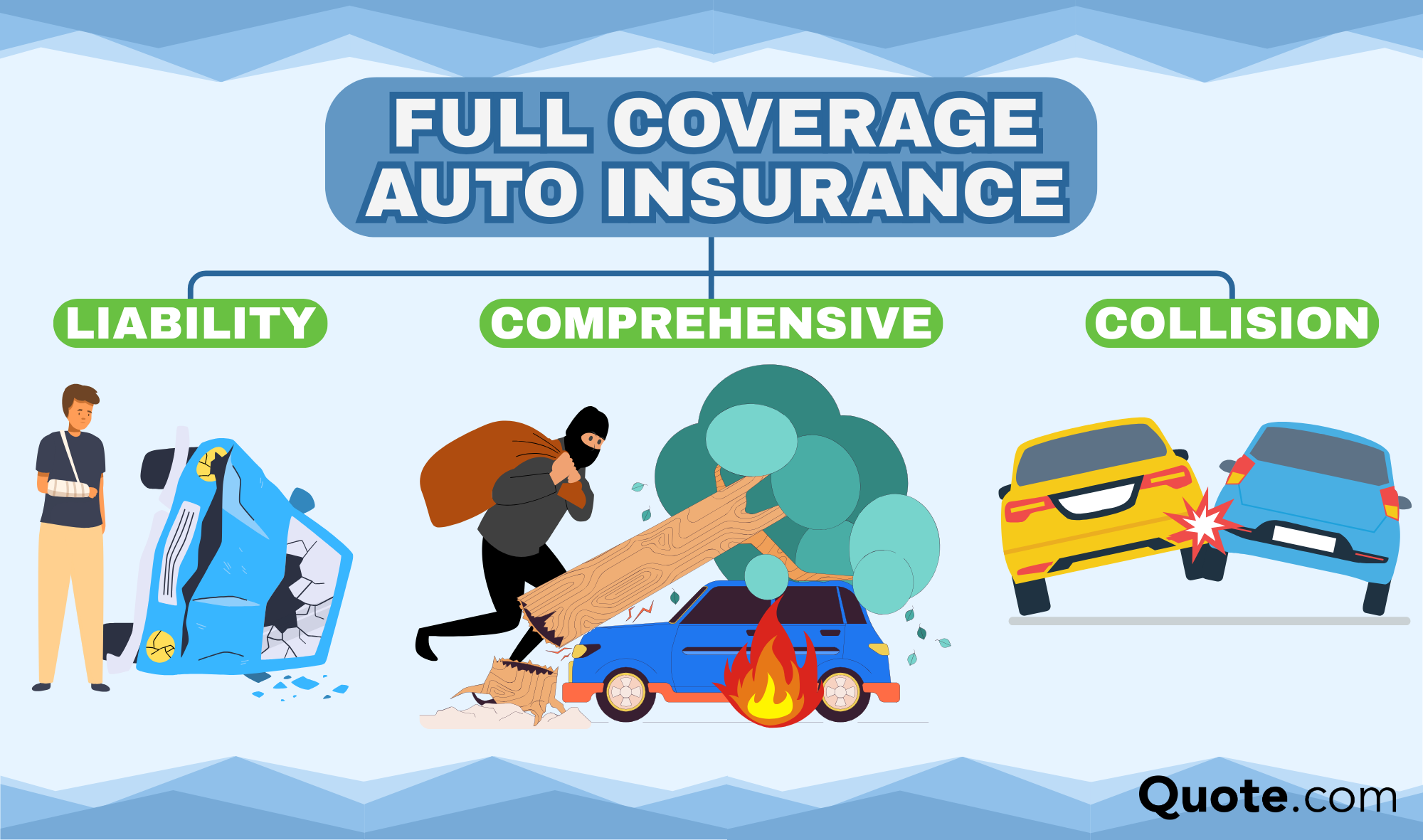

Comprehensive Car Cover Basics

Comprehensive car coverage protects against damage not caused by a collision. It covers theft, vandalism, fire, natural disasters, and falling objects. This type of insurance helps pay for repairs or replacement when your car faces these risks. It also covers windshield damage and animal collisions.

Comprehensive coverage is different from full coverage. Full coverage usually means comprehensive plus collision insurance. Collision insurance pays for damage from crashes with other vehicles or objects. Comprehensive does not cover crash damage.

Common misconceptions include thinking comprehensive covers everything. It does not cover mechanical problems or normal wear and tear. Also, it is not the same as liability insurance, which pays for damage to others if you cause an accident.

Benefits Of Comprehensive Car Cover

Comprehensive car cover protects your vehicle from theft and vandalism. It helps pay for repairs or replacement if your car is stolen or damaged by others. This coverage gives peace of mind in busy or unsafe areas.

Natural disasters like floods, hail, or storms can damage your car. Comprehensive cover helps fix or replace your vehicle after such events. It saves you from paying large repair bills out of pocket.

Accidental damage benefits cover unexpected events like hitting a pole or crashing into something. This insurance pays for repairs that other policies might not cover. It helps keep your car safe and your finances secure.

How To Compare Comprehensive Car Covers

Compare comprehensive car covers by checking key features carefully. Start by understanding policy limits. These tell how much the insurer will pay for a claim. Also, read the exclusions. Exclusions show what is not covered. This helps avoid surprises later.

Next, look at the deductibles. This is the amount you pay before insurance helps. A lower deductible means higher premium, but less out-of-pocket cost in a claim. A higher deductible lowers the premium but costs more if you claim.

Compare coverage details side by side. Check if the policy covers theft, fire, natural disasters, and vandalism. Some policies offer extras like roadside assistance or rental car coverage. These can add value to your insurance.

Top Providers And Their Offers

Major insurance companies offer various comprehensive car cover plans. These include well-known firms like State Farm, GEICO, Progressive, and Allstate. Each provider has unique features and discounts to lower your premium. Common discounts cover safe driving, multiple policies, and vehicle safety devices.

Customer service quality and the claims process differ widely. Some companies provide 24/7 claims support and fast settlements. Others may require longer processing times or more documentation. Checking reviews can help pick a reliable insurer.

| Provider | Special Features | Discounts | Claims Process |

|---|---|---|---|

| State Farm | Accident forgiveness, Roadside assistance | Safe driver, Multi-car | Fast, 24/7 support |

| GEICO | Rental car coverage, Mechanical breakdown | Good student, Military | Online claims, quick response |

| Progressive | Snapshot usage-based program | Multi-policy, Safe vehicle | Mobile app claims, easy filing |

| Allstate | Safe driving bonus, New car replacement | Multi-line, Safe driver | Personal claims agent, fast service |

Cost Considerations

In Austin, Texas, the average comprehensive car insurance premium usually ranges from $1,200 to $1,800 per year. Rates vary widely based on different factors like driving history and coverage limits. Urban areas like Austin often have higher rates due to traffic and theft risks.

Vehicle type impacts premiums significantly. Sports cars and luxury vehicles cost more to insure. Larger vehicles like trucks might have higher rates due to repair costs. Older cars can be cheaper, but some models might lack parts, increasing costs.

- Increase your deductible to lower premiums.

- Bundle insurance policies to get discounts.

- Maintain a good driving record to avoid surcharges.

- Ask about discounts for safety features on your vehicle.

Smart Protection Tips

Regularly review your car insurance policy to ensure it fits your current needs. Your driving habits and car value may change over time. Check your coverage limits and deductibles to avoid surprises during claims.

Bundling insurance policies like home and auto can save money. Many insurers offer discounts when you combine multiple policies. This also simplifies managing your insurance with a single provider.

Use technology to improve car safety. Installing GPS trackers, dash cams, or alarm systems can reduce theft risk. Some insurers offer discounts for using these devices, which show you take safety seriously.

Frequently Asked Questions

What Not To Tell Your Insurance Company?

Avoid giving false information, admitting fault, or hiding prior claims. Don’t disclose unrelated medical history or unnecessary personal details. Stay factual and concise to protect your coverage and claim approval.

Is Comprehensive Cover The Same As Fully Comprehensive?

Comprehensive cover and fully comprehensive mean the same. Both protect against damage, theft, and third-party claims beyond basic liability.

Is It Better To Have A $500 Deductible Or $1000?

Choosing a $500 deductible means higher monthly premiums but lower out-of-pocket costs after a claim. A $1000 deductible lowers premiums but increases your payment during claims. Select based on your budget and risk tolerance for better savings or lower immediate costs.

Is 50/100/50 Good Insurance Coverage?

50/100/50 coverage meets minimum liability requirements in many states. It offers basic protection but may be insufficient for serious accidents. Consider higher limits for better financial security and to cover medical and property damage costs fully. Always evaluate your personal risk and state laws.

Conclusion

Choosing the right comprehensive car cover protects your vehicle and your wallet. Comparing options helps find the best price and coverage. Focus on what matters most: damage protection, theft, and natural events. Check each policy’s limits and exclusions carefully before deciding.

Taking time to compare saves money and stress in the long run. Stay informed, stay protected, and drive with peace of mind.

Read More

- Family Car Insurance Discount: Save Big with These Proven Tips

- Low Mileage Auto Insurance Rates: Save Big with Smart Discounts

- Roadside Assistance Insurance Plans: Essential Coverage for Peace of Mind

- Affordable Vehicle Insurance Quotes: Save Big with Top Tips Today

- Paint Protection Film Cost: Ultimate Guide to Affordable Shielding

- Wheel And Tire Protection Plan: Ultimate Coverage for Peace of Mind

- Windshield Protection Insurance: Ultimate Guide to Save & Secure

- Vehicle Theft Protection Coverage: Ultimate Guide to Secure Your Car

- Powertrain Warranty Coverage: Ultimate Protection for Your Vehicle

- Certified Used Car Warranty: Ultimate Protection for Peace of Mind